01 Feb Retirement Plan Limits for 2025

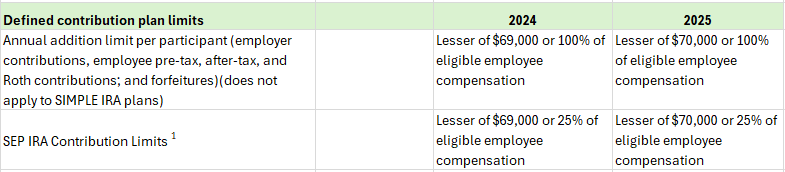

Note: Elective salary deferrals and catch-up contributions are not permitted in SEP plans.

1 If you are self-employed, your effective contribution rate is closer to 20% of net self-employment income. Contributions are based on your net earnings from self-employment (after deducting half of your self-employment tax and your own SEP contributions). You can use this IRS link to determine contributions for yourself.

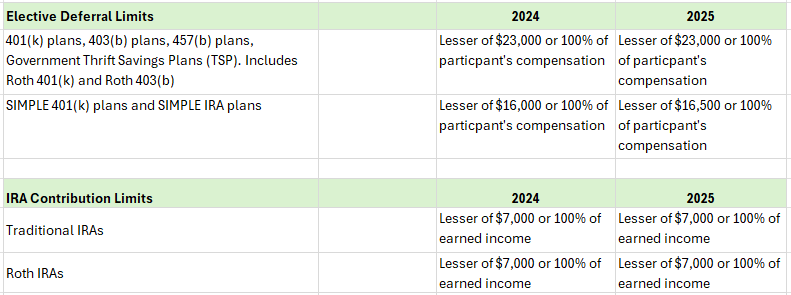

Note that Roth IRA compensation limits do not apply to a Roth 401(k).

Contributions to a Roth 401(k) are only subject to the plan’s deferral limits, not to income-based restrictions like those for Roth IRA.

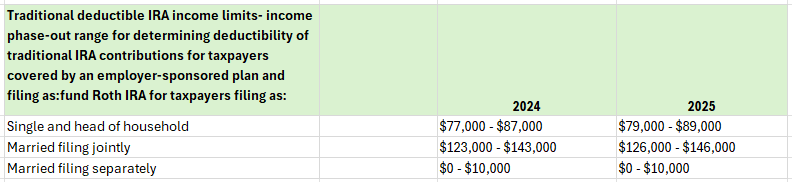

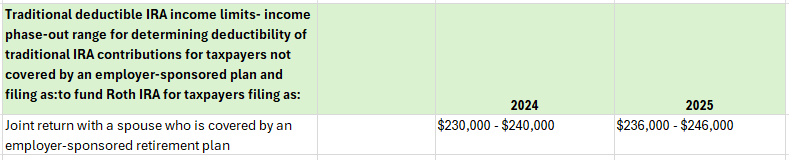

For example, for a single filer, there would be a full deduction $79,000 or less; No deduction if $89,000 or more. Based of Modified Adjusted Gross Income (MAGI)

This information is general in nature, is not a complete statement of all information necessary for making an investment decision and is not a recommendation or a solicitation to buy or sell any security. Investments and strategies mentioned may not be suitable for all investors. Past performance may not be indicative of future results.

Prepared by Heart Strong Wealth Planning