19 Nov Company Stock and Your Retirement Strategy

The opportunity to acquire company stock — inside or outside a workplace retirement plan — can be a lucrative employee benefit. Your compensation may include stock options or bonuses paid in company stock. Shares may be offered at a discount through an employee stock purchase plan and held in a taxable account, or company stock might be one of the investment options in your tax-deferred 401(k) plan.

Either way, having too much of your retirement savings or net worth invested in your employer’s stock could become a problem if the company or sector hits hard times, especially if a job loss and stock value loss occur at the same time. There are also tax implications to consider.

Concentrate on Diversification

The possibility of heavy losses from having a large portion of your portfolio holdings in one investment, asset class, or market segment is known as concentration risk. Buying shares of any individual stock carries risks s

Holding more than 10% to 15% of your assets in company stock could upend your retirement strategy if the stock suddenly declines in value, and overconcentration can sneak up on you as your position builds slowly over time. To help maintain a healthy level of diversification in your portfolio, look closely at your plan’s investment options and consider directing some of your contributions into funds that provide exposure to a wider variety of market sectors.

You might also consider strategies that involve selling company shares systematically or right after they become vested. But make sure you are aware of the rules, restrictions, and time frames for liquidating company stock, as well as any tax consequences.

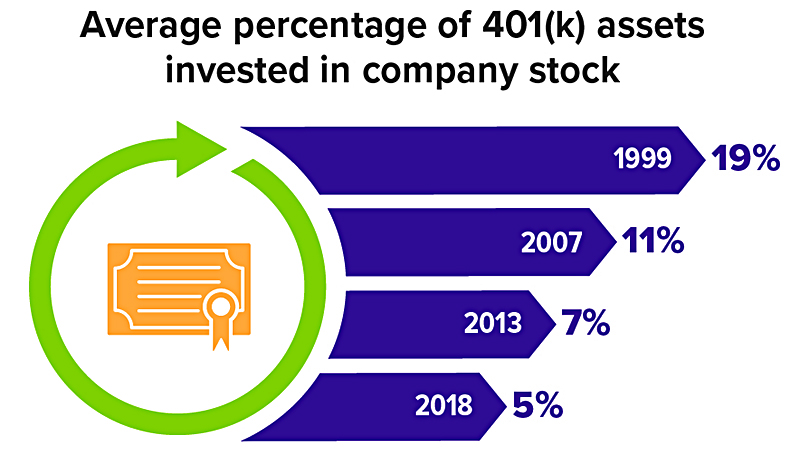

Company Stock Ownership Has Fallen

Source: Employee Benefit Research Institute, 2021 (data from participants in the 2018 EBRI/ICI 401(k) database)

Take Advantage of NUA

If you sell stock inside your 401(k) account and reinvest in other plan options, or you roll the stock over to an IRA, future distributions will likely be taxed as ordinary income. However, if you own highly appreciated company stock in your employer plan, you might benefit from a special tax break on lump-sum distributions of net unrealized appreciation (NUA). NUA allows the appreciation on company stock in a 401(k) to be taxed at lower long-term capital gains rates when the shares are sold, instead of the ordinary income tax rates that would otherwise apply to retirement plan distributions.

To qualify for NUA, the lump-sum distribution must follow a triggering event such as separation from service, reaching age 59½, disability, or death. The stock must be distributed in kind — as stock — and transferred to a taxable account. You would owe income tax at the ordinary rate in the year of the distribution, but only on the cost basis of the stock.

If your retirement plan consists of employer stock and other types of investments (cash, mutual funds, etc.), the other assets can be transferred into an IRA, to another employer’s plan, or withdrawn entirely. This doesn’t have to happen simultaneously with the stock distribution, but the distributions must occur in the same tax year, and the account balance on your employer plan must be zero by the end of that year.

If distributions of company stock are handled correctly, the savings from NUA can be substantial, especially for those in higher tax brackets. But keep in mind that taking any partial distribution from your employer plan after a triggering event — even an in-plan Roth conversion or required minimum distribution — could disqualify you from the NUA tax break, unless another triggering event occurs.

All investments are subject to market fluctuation, risk, and loss of principal. When sold, investments may be worth more or less than their original cost. Diversification and asset allocation are methods used to help manage investment risk; they do not guarantee a profit or protect against investment loss.

This information is general in nature, is not a complete statement of all information necessary for making an investment decision, and is not a recommendation or a solicitation to buy or sell any security. Investments and strategies mentioned may not be suitable for all investors. Past performance may not be indicative of future results.

©️️ Meredith D Sims 2021. Prepared by Heart Strong Wealth Planning.