24 Nov Is a High-Deductible Health Plan Right for You?

In 2020, 31% of U.S. workers with employer-sponsored health insurance had a high-deductible health plan (HDHP), up from 24% in 2015.1 These plans are also available outside the workplace through private insurers and the Health Insurance Marketplace.

In 2020, 31% of U.S. workers with employer-sponsored health insurance had a high-deductible health plan (HDHP), up from 24% in 2015.1 These plans are also available outside the workplace through private insurers and the Health Insurance Marketplace.

Although HDHP participation has grown rapidly, the most common plan — covering almost half of U.S. workers — is a traditional preferred provider organization (PPO).2 If you are thinking about enrolling in an HDHP or already enrolled in one, here are some factors to consider when comparing an HDHP to a PPO.

Up-Front Savings

The average annual employee premium for HDHP family coverage in 2020 was $4,852 versus $6,017 for a PPO, a savings of $1,165 per year.3 In addition, many employers contribute to a health savings account (HSA) for the employee, and contributions by the employer or the employee are tax advantaged (see below). Taken together, these features could add up to substantial savings that can be used to pay for current and future medical expenses.

Pay As You Go

In return for lower premiums, you pay more out of pocket for medical services with an HDHP until you reach the annual deductible.

Deductible. An HDHP has a higher deductible than a PPO, but PPO deductibles have been rising, so consider the difference between plan deductibles and whether the deductible is per person or per family. PPOs may have a separate deductible (or no deductible) for prescription drugs, but the HDHP deductible will apply to all covered medical spending.

Copays. PPOs typically have copays that allow you to obtain certain services and prescription drugs with a defined payment before meeting your deductible. With an HDHP, you pay out of pocket until you meet your deductible, but costs may be reduced through the insurer’s negotiated rate. Consider the difference between the copay and the negotiated rate for a typical service such as a doctor visit. Certain types of preventive care and preventive medicines may be provided at no cost under both types of plans.

Maximums. Most health insurance plans have annual and lifetime out-of-pocket maximums above which the insurer pays all medical expenses. HDHP maximums may be the same or similar to that of PPO plans. (Some PPO plans have a separate annual maximum for prescription drugs.) If you have high medical costs that exceed the annual maximum, your total out-of-pocket costs for that year would typically be lower for an HDHP with the savings on premiums.

Your Choices and Preferences

Both PPOs and HDHPs offer incentives to use health-care providers within a network, and the network may be exactly the same if the plans are offered by the same insurance company. Make sure your preferred doctors are included in the network before enrolling.

Also consider whether you are comfortable using the HDHP structure. Although it may save money over the course of a year, you might be hesitant to obtain appropriate care because of the higher out-of-pocket expense at the time of service.

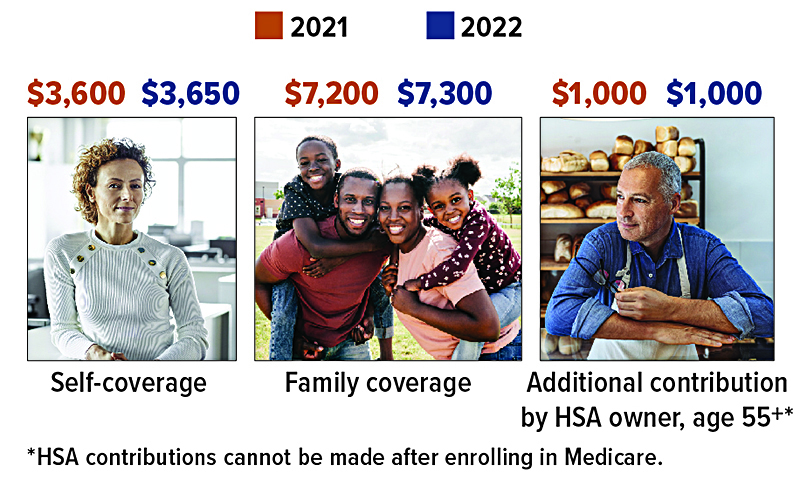

HSA Contribution Limits

Annual contributions can be made up to the April tax filing deadline of the following year. Any employer contributions must be considered as part of the annual limit.

Health Savings Accounts

High-deductible health plans are designed to be paired with a tax-advantaged health savings account (HSA) that can be used to pay medical expenses incurred after the HSA is established. HSA contributions are typically made through pre-tax payroll deductions, but in most cases they can also be made as tax-deductible contributions directly to the HSA provider. HSA funds, including any earnings if the account has an investment option, can be withdrawn free of federal income tax and penalties as long as the money is spent on qualified health-care expenses. (Some states do not follow federal tax rules on HSAs.)

The assets in an HSA can be retained in the account or rolled over to a new HSA if you change employers or retire. Unspent HSA balances can be used to pay future medical expenses whether you are enrolled in an HDHP or not; however, you must be enrolled in an HDHP to establish and contribute to an HSA.

1–3) Kaiser Family Foundation, 2020

This information is general in nature, is not a complete statement of all information necessary for making an investment decision, and is not a recommendation or a solicitation to buy or sell any security. Investments and strategies mentioned may not be suitable for all investors. Past performance may not be indicative of future results.

Prepared by Broadridge Advisor Solutions Copyright 2021.