25 Sep Why Buy Life Insurance During Unsettled Economic Times?

To say the economy has been uneven over the past few years is an understatement. Amid these bumpy economic times, why buy life insurance? Here are a few reasons.

Protection for Loved Ones

Savings that were intended to provide support for you and your family may have taken a hit over the past few years due to stock market volatility. If you die, life insurance can be used to replace some of the savings you may have lost during these turbulent economic times. The tax-free death benefit could be used to provide income to your spouse and family, pay off mortgages and loans, meet tax liabilities, or pay for college expenses.

May Help Diversify Your Portfolio

Certain types of permanent life insurance have a cash value option that can be beneficial during times of economic uncertainty. Some policies offer minimum interest rate guarantees (subject to the financial strength and claims-paying ability of the issuer), that may offer an alternative to the unpredictability of the stock market.

Offers an Additional Way to Accumulate Wealth

Cash value life insurance allows all interest and earnings on the policy’s accumulations to grow tax deferred. You may be able to take withdrawals from the cash accumulation of the life insurance policy. Any withdrawal you make will typically be tax-free up to your basis (i.e., premiums paid) in the policy. Because any earnings grow tax deferred while inside the policy, they will be subject to income tax when you withdraw them. Withdrawals coming out of your policy are generally treated as basis first. Be aware that surrender charges may also apply when you withdraw from your policy, even if you withdraw only up to your basis. One way to avoid this and still access your money is to take a policy loan from the insurance company, using the cash value in the policy as collateral. The amount you borrow is generally not treated as taxable income as long as you repay the loan, and there are no surrender charges because you’re not actually withdrawing your money. But you’ll have to pay interest on the loan, which is not tax deductible.

Provides Protection in the Form of Living Benefits

Life insurance may help replace lost funds should you become disabled, need long-term care, or face a terminal illness. For example, if you are terminally ill, you may be able to receive a portion of the death proceeds from your life insurance before you die in order to pay necessary expenses. Some life insurance policies include a special rider that allows you to accelerate your life insurance death benefit if you need long-term care during your life. Certain riders can be added to a life insurance policy and may help in the event you become disabled and unable to work.

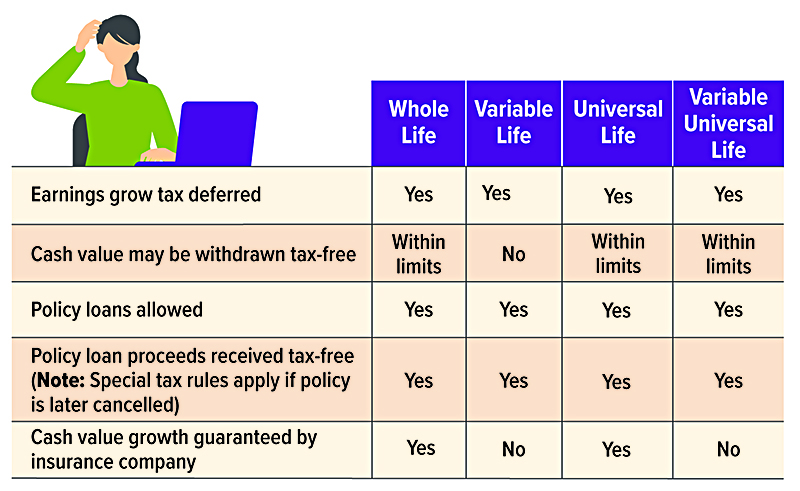

Comparison of Types of Cash Value Life Insurance

Optional benefit riders are available for an additional fee and are subject to contractual terms, conditions and limitations as outlined in the policy and may not benefit all investors. Any payments used for covered long-term care expenses would reduce (and are limited to) the death benefit or annuity value and can be much less than those of a typical long-term care policy. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Any guarantees are subject to the financial strength and claims-paying ability of the insurance issuer. The investment return and principal value of the variable investment options will fluctuate and are not guaranteed. Loans and withdrawals from a permanent life insurance policy will reduce the policy’s cash value and death benefit, could increase the chance that the policy will lapse, and might result in a tax liability if the policy terminates before the death of the insured. Additional out-of-pocket payments may be needed if actual dividends or investment returns decrease, if you withdraw policy cash values, or if current charges increase.

This information is general in nature, is not a complete statement of all information necessary for making an investment decision and is not a recommendation or a solicitation to buy or sell any security. Investments and strategies mentioned may not be suitable for all investors. Past performance may not be indicative of future results.

Prepared by Broadridge Advisor Solutions Copyright 2023.